To Learn More, Be Sure to Visit - oceancityfinancialgroup.com

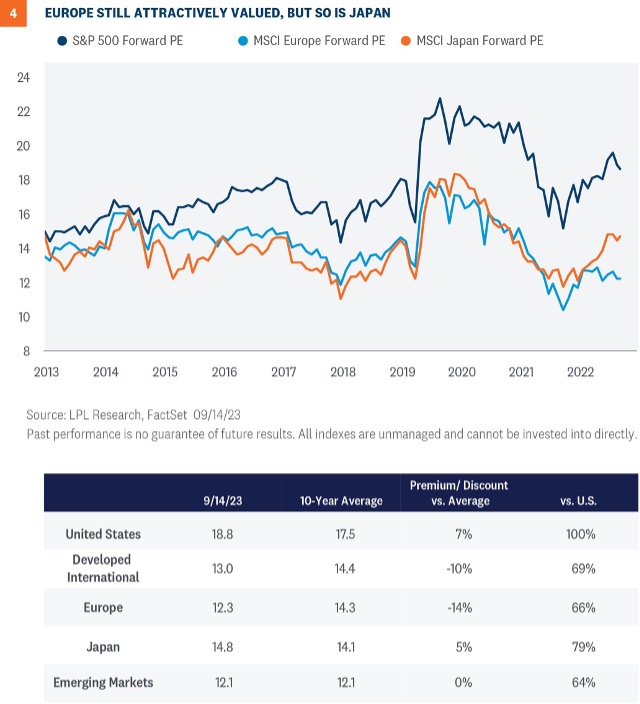

Jeffrey Buchbinder, CFA, Chief Equity Strategist Jeffrey Roach, PhD, Chief Economist Recent data suggests economic conditions in Europe are deteriorating, removing a key element of LPL Research’s positive view of the attractively valued developed international equities asset class. Previous U.S. dollar weakness and strong earnings momentum, which were other key reasons why we became more interested in European investing earlier this year, have reversed and suggest looking elsewhere for investment opportunities. Another international market to consider is Japan, which is also attractively valued with better fundamentals than Europe, in our view.

Recent data suggests economic conditions in Europe are deteriorating, removing a key element of LPL Research’s positive view of the attractively valued developed international equities asset class. Previous U.S. dollar weakness and strong earnings momentum, which were other key reasons why we became more interested in European investing earlier this year, have reversed and suggest looking elsewhere for investment opportunities. Another international market to consider is Japan, which is also attractively valued with better fundamentals than Europe, in our view.

Turning to a more commonly used economic measure, Eurozone GDP for the second quarter was revised down to a 0.1% expansion from the previous 0.3% estimate, which pales in comparison to what the U.S. (+2.1% annualized) and Japan (+4.8%) produced during the second quarter. So, while growth is also expected to slow in the U.S. and Japan, Europe has much less economic momentum to help carry the region through the next six to 12 months as the impact of tighter monetary policy is increasingly felt. As a result, economic activity in the Eurozone will likely be subdued for the rest of the year and into 2024.

Getting more granular and taking a look at individual countries, we see the outlook is hazy for countries like the United Kingdom (U.K.) and Germany. The U.K.’s economy contracted 0.5% month over month in July. This pace of contraction is the worst seen in seven months, with every major sector of the economy declining during the month. Although still suffering from prolonged inflation and higher borrowing costs, labor action took a heavy toll as education and health employees went on strike. Investors should know that such a sharp contraction raises the possibility of a potential recession in the U.K. as 2023 draws to a close.

Moving over to Germany, the ZEW Economic Sentiment Index showed investors are still not confident in an economic turnaround in the next six months. September’s index fell to -11.4, well below the 0 threshold that separates bullish and bearish sentiments. Investors cited instability caused by conflict and unusual climate episodes, as well as inflation and decreased manufacturing output. Near-term risks are rising for the biggest economy in Europe.

Global central bankers are in a tough spot, but among major central banks, none look tougher than the job facing Christine Lagarde at the European Central Bank (ECB). Inflation remains stubbornly high in Europe, which triggered the ECB’s decision to hike rates a quarter point on September 14—its tenth straight meeting with a rate hike—despite the sluggish economy.

Meanwhile, U.S. markets are still unsure if the Federal Reserve (Fed) is completely done, but unlike Europe, the domestic economy remains resilient, and U.S. inflation is on a better trajectory than its European counterparts. Meanwhile, Japan’s economy grew like gangbusters the past two quarters, and the Bank of Japan (BOJ) has barely started withdrawing its accommodative monetary policy. The BOJ has signaled its intention to remove its yield curve control (YCC) program, but the timetable is uncertain.

Europe faces energy, labor, and geopolitical headwinds and lacks the innovation engine that can propel stronger growth like the U.S., and, to a lesser extent, Japan, enjoys.

Turning to a more commonly used economic measure, Eurozone GDP for the second quarter was revised down to a 0.1% expansion from the previous 0.3% estimate, which pales in comparison to what the U.S. (+2.1% annualized) and Japan (+4.8%) produced during the second quarter. So, while growth is also expected to slow in the U.S. and Japan, Europe has much less economic momentum to help carry the region through the next six to 12 months as the impact of tighter monetary policy is increasingly felt. As a result, economic activity in the Eurozone will likely be subdued for the rest of the year and into 2024.

Getting more granular and taking a look at individual countries, we see the outlook is hazy for countries like the United Kingdom (U.K.) and Germany. The U.K.’s economy contracted 0.5% month over month in July. This pace of contraction is the worst seen in seven months, with every major sector of the economy declining during the month. Although still suffering from prolonged inflation and higher borrowing costs, labor action took a heavy toll as education and health employees went on strike. Investors should know that such a sharp contraction raises the possibility of a potential recession in the U.K. as 2023 draws to a close.

Moving over to Germany, the ZEW Economic Sentiment Index showed investors are still not confident in an economic turnaround in the next six months. September’s index fell to -11.4, well below the 0 threshold that separates bullish and bearish sentiments. Investors cited instability caused by conflict and unusual climate episodes, as well as inflation and decreased manufacturing output. Near-term risks are rising for the biggest economy in Europe.

Global central bankers are in a tough spot, but among major central banks, none look tougher than the job facing Christine Lagarde at the European Central Bank (ECB). Inflation remains stubbornly high in Europe, which triggered the ECB’s decision to hike rates a quarter point on September 14—its tenth straight meeting with a rate hike—despite the sluggish economy.

Meanwhile, U.S. markets are still unsure if the Federal Reserve (Fed) is completely done, but unlike Europe, the domestic economy remains resilient, and U.S. inflation is on a better trajectory than its European counterparts. Meanwhile, Japan’s economy grew like gangbusters the past two quarters, and the Bank of Japan (BOJ) has barely started withdrawing its accommodative monetary policy. The BOJ has signaled its intention to remove its yield curve control (YCC) program, but the timetable is uncertain.

Europe faces energy, labor, and geopolitical headwinds and lacks the innovation engine that can propel stronger growth like the U.S., and, to a lesser extent, Japan, enjoys.

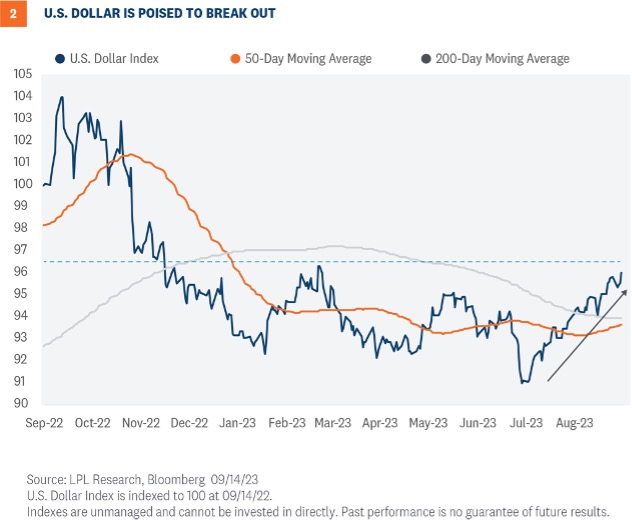

The other side of the story is European exporters should garner some support from a weaker currency (making their goods more attractive to U.S. buyers). Regardless, even though the case for USD weakness over the intermediate and longer term looks like a strong one, our conviction in calling a short term dollar decline is low, removing a potential boost for European equities.

The other side of the story is European exporters should garner some support from a weaker currency (making their goods more attractive to U.S. buyers). Regardless, even though the case for USD weakness over the intermediate and longer term looks like a strong one, our conviction in calling a short term dollar decline is low, removing a potential boost for European equities.

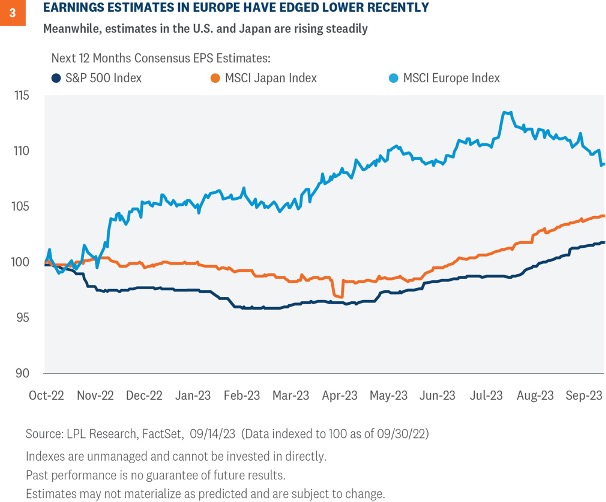

With recession increasingly likely in Europe in the near term, particularly in Germany, the current consensus expectation for 6% earnings growth from MSCI Europe in 2024 may be too high—though we acknowledge the 12% earnings growth reflected in S&P 500 consensus is also too high. Regardless, we would anticipate the U.S. and Japan delivering stronger earnings growth than Europe over the rest of this year and in 2024.

With recession increasingly likely in Europe in the near term, particularly in Germany, the current consensus expectation for 6% earnings growth from MSCI Europe in 2024 may be too high—though we acknowledge the 12% earnings growth reflected in S&P 500 consensus is also too high. Regardless, we would anticipate the U.S. and Japan delivering stronger earnings growth than Europe over the rest of this year and in 2024.

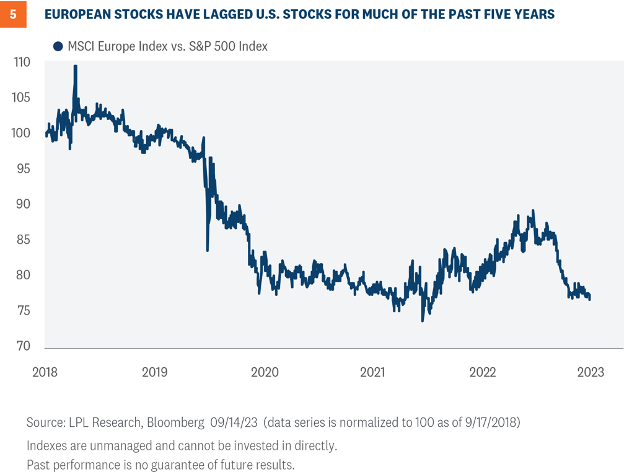

Importantly, Europe’s sector mix has much less technology, making it difficult to keep up with the U.S. The MSCI Europe Index has just a 6.6% weighting in technology, compared to more than four times that amount (27.7%) in the U.S. Although the technology sector’s 40% year-to- date rally may be a bit overdone, in rising markets it’s tough for European markets with a more defensive sector mix to keep up.

Importantly, Europe’s sector mix has much less technology, making it difficult to keep up with the U.S. The MSCI Europe Index has just a 6.6% weighting in technology, compared to more than four times that amount (27.7%) in the U.S. Although the technology sector’s 40% year-to- date rally may be a bit overdone, in rising markets it’s tough for European markets with a more defensive sector mix to keep up.

INVESTMENT CONCLUSION

INVESTMENT CONCLUSION Ocean City Financial Group

Mark R. Reimet CFP®

801 ASBURY AVENUE

SUITE 650

OCEAN CITY, NJ 08226

609-814-1100 Office

[email protected]

OceanCityFinancialGroup.com

Securities and advisory services offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC. LPL Financial and Ocean City Financial Group are separate entities.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability.

Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency

Not Bank/Credit Union Guaranteed

Not Bank/Credit Union Deposits or Obligations

May Lose Value

RES-1627733-0823 | For Public Use | Tracking # 479826 (Exp. 09/2024)

For a list of descriptions of the indexes referenced in this publication, please visit our website at lplresearch.com/definitions.

Ocean City Financial Group

Mark R. Reimet CFP®

801 ASBURY AVENUE

SUITE 650

OCEAN CITY, NJ 08226

609-814-1100 Office

[email protected]

OceanCityFinancialGroup.com

Securities and advisory services offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC. LPL Financial and Ocean City Financial Group are separate entities.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability.

Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency

Not Bank/Credit Union Guaranteed

Not Bank/Credit Union Deposits or Obligations

May Lose Value

RES-1627733-0823 | For Public Use | Tracking # 479826 (Exp. 09/2024)

For a list of descriptions of the indexes referenced in this publication, please visit our website at lplresearch.com/definitions.