To Learn More, Be Sure to Visit - oceancityfinancialgroup.com

Jeffrey Buchbinder, CFA, Chief Equity Strategist, LPL Financial Thomas Shipp, CFA, Quantitative Equity Analyst Fourth quarter earnings season is underway and probably won’t bring much good news. Lackluster global growth, ongoing profit margin pressures from inflation, and negative currency impacts are likely to translate into a year-over-year decline in S&P 500 Index earnings for the quarter. As always, guidance matters more as market participants look forward. The key question coming into this earnings season is whether the pessimism surrounding 2023 earnings has gone too far.

A NUMBER OF HEADWINDS

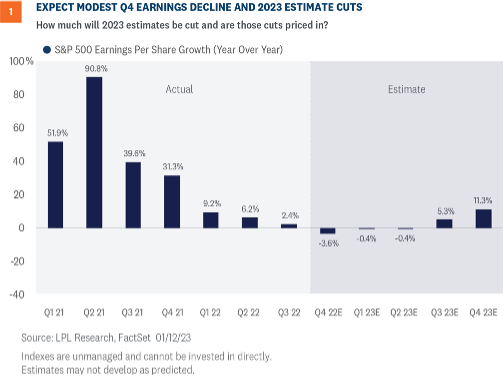

As was the case last quarter, corporate America faces several stiff headwinds this earnings season. These headwinds—clearly not new news—include slower global economic growth, cost pressures from still-elevated inflation, ongoing supply chain issues, currency drag from a stronger U.S. dollar last quarter compared with the year-ago quarter, and geopolitical instability, particularly in Eastern Europe and China. These headwinds will likely translate into a slight year-over-year (YOY) earnings decline for the S&P 500 in the fourth quarter, with an outside shot at getting above the flat line (Figure 1). Consensus currently stands at -3.6% YOY in the quarter (source: FactSet).

Fourth quarter earnings season is underway and probably won’t bring much good news. Lackluster global growth, ongoing profit margin pressures from inflation, and negative currency impacts are likely to translate into a year-over-year decline in S&P 500 Index earnings for the quarter. As always, guidance matters more as market participants look forward. The key question coming into this earnings season is whether the pessimism surrounding 2023 earnings has gone too far.

A NUMBER OF HEADWINDS

As was the case last quarter, corporate America faces several stiff headwinds this earnings season. These headwinds—clearly not new news—include slower global economic growth, cost pressures from still-elevated inflation, ongoing supply chain issues, currency drag from a stronger U.S. dollar last quarter compared with the year-ago quarter, and geopolitical instability, particularly in Eastern Europe and China. These headwinds will likely translate into a slight year-over-year (YOY) earnings decline for the S&P 500 in the fourth quarter, with an outside shot at getting above the flat line (Figure 1). Consensus currently stands at -3.6% YOY in the quarter (source: FactSet).

The good news is some of these pressures have started to abate, particularly currency pressures, after a 9% drop in the U.S. dollar since the fourth quarter began on October 1 (though it was up about 6% YOY in Q4). Even the economic pressures have eased some, with fourth quarter U.S. gross domestic product (GDP) likely to exceed the 1.2% consensus forecast of economists surveyed by Bloomberg based on the latest data. And don’t forget the

U.S. economy grew at a solid 3.2% pace in the third quarter of 2022, while Europe has held up better than we anticipated, thanks in large part to falling natural gas prices.

Bottom line, if we’re going to get enough upside for the S&P 500 to grow earnings at all in Q4, it will likely come from the resilience of the U.S. and European economies, currency effects, and some mitigation of profit margin pressures from cost controls and lower inflation.

The good news is some of these pressures have started to abate, particularly currency pressures, after a 9% drop in the U.S. dollar since the fourth quarter began on October 1 (though it was up about 6% YOY in Q4). Even the economic pressures have eased some, with fourth quarter U.S. gross domestic product (GDP) likely to exceed the 1.2% consensus forecast of economists surveyed by Bloomberg based on the latest data. And don’t forget the

U.S. economy grew at a solid 3.2% pace in the third quarter of 2022, while Europe has held up better than we anticipated, thanks in large part to falling natural gas prices.

Bottom line, if we’re going to get enough upside for the S&P 500 to grow earnings at all in Q4, it will likely come from the resilience of the U.S. and European economies, currency effects, and some mitigation of profit margin pressures from cost controls and lower inflation.

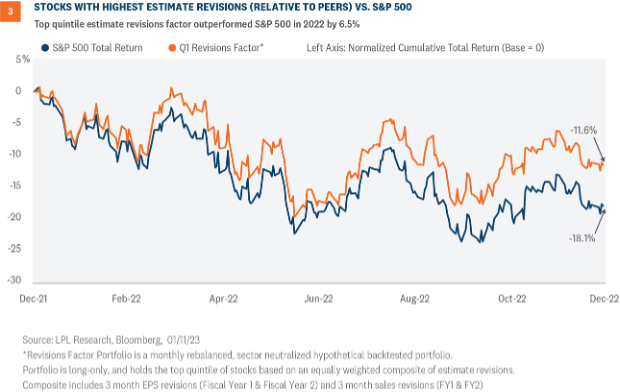

Here are some reasons why estimate cuts may not be as drastic as some fear:

Here are some reasons why estimate cuts may not be as drastic as some fear:

CONCLUSION

This earnings season likely won’t offer much in the way of good news. We saw that in the challenges the banks faced in their reports on Friday, January 13 (an inauspicious date to start earnings season). But pessimism may be overdone, and investors may be surprised at how well stocks hold up on the news. Look for earnings throughout the next year to exceed those pessimistic forecasts and—along with falling inflation and the end of Federal Reserve rate hikes—serve as positive catalysts for solid gains for stocks in 2023.

CONCLUSION

This earnings season likely won’t offer much in the way of good news. We saw that in the challenges the banks faced in their reports on Friday, January 13 (an inauspicious date to start earnings season). But pessimism may be overdone, and investors may be surprised at how well stocks hold up on the news. Look for earnings throughout the next year to exceed those pessimistic forecasts and—along with falling inflation and the end of Federal Reserve rate hikes—serve as positive catalysts for solid gains for stocks in 2023.

Ocean City Financial Group

Mark R. Reimet CFP®

801 ASBURY AVENUE

SUITE 650

OCEAN CITY, NJ 08226

609-814-1100 Office

[email protected]

OceanCityFinancialGroup.com

Securities and advisory services offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC. LPL Financial and Ocean City Financial Group are separate entities.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability.

Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency

Not Bank/Credit Union Guaranteed

Not Bank/Credit Union Deposits or Obligations

May Lose Value

RES-1390600-0123 | For Public Use | Tracking # 1-05356048 (Exp. 01/24)

For a list of descriptions of the indexes referenced in this publication, please visit our website at lplresearch.com/definitions.

Ocean City Financial Group

Mark R. Reimet CFP®

801 ASBURY AVENUE

SUITE 650

OCEAN CITY, NJ 08226

609-814-1100 Office

[email protected]

OceanCityFinancialGroup.com

Securities and advisory services offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC. LPL Financial and Ocean City Financial Group are separate entities.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability.

Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency

Not Bank/Credit Union Guaranteed

Not Bank/Credit Union Deposits or Obligations

May Lose Value

RES-1390600-0123 | For Public Use | Tracking # 1-05356048 (Exp. 01/24)

For a list of descriptions of the indexes referenced in this publication, please visit our website at lplresearch.com/definitions.