To Learn More, Be Sure to Visit - oceancityfinancialgroup.com

Jeffrey Buchbinder, CFA,

Chief Equity Strategist

Adam Turnquist, CMT, Chief Technical Strategist

Following the Federal Reserve’s (Fed) aggressive rate-hiking campaign in 2022 and 2023, stocks are entering a phase in which the market narrative is focused on interest-rate stability — as inflation, we believe, comes down further. Low and stable interest rates should help support stock valuations, while corporate profits are moving into a sweet spot. So even though stocks look fully valued, if rates ease as we expect, we could see upside to our year-end 2024 fair-value target range of 4,850 to 4,950. We highlight some key themes for stocks next year.

MORE SUPPORTIVE ECONOMIC ENVIRONMENT

If 2023 was the year of stubbornly high inflation and rate hikes, perhaps 2024 could be the year of significant progress toward the Fed’s 2% inflation target and rate cuts.

This economic cycle has been unique and difficult to predict due to post-pandemic distortions. Importantly, though, even if we get a mild, short-lived recession in the first half of 2024 (far from assured), a second-half 2024 economic recovery should support stocks. We believe the bear market in 2022 and accompanying cost cuts from corporate America (particularly in technology areas) prepared markets for a slowdown, which should help mitigate equity market downside. And don’t forget, the inflation and rate surge that sparked recession fears is far less of a worry today.

So, while the uncertainty that comes with anticipating a recession may limit stock gains in early 2024, it could bolster investor sentiment midyear, as is typical coming out of an economic trough (the lowest part and turning point of an economic cycle). Bottom line, we anticipate a stock- market-friendly macroeconomic environment in 2024, and one in which bonds may also perform quite well.

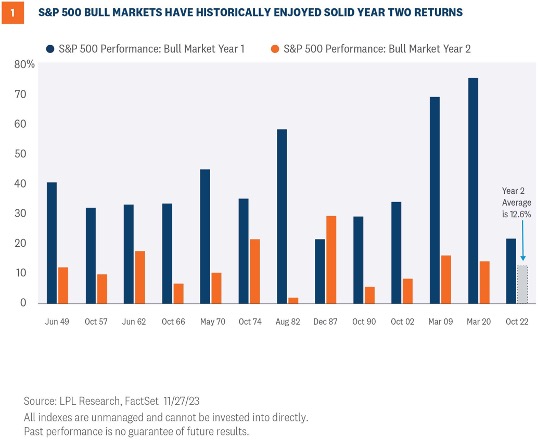

THIS BULL MARKET IS STILL YOUNG

History doesn’t always repeat, but it rhymes. As the next 12 months of the bull market get underway, kicking off year two of this bull market born in late 2022, market history tells us solid gains may lie ahead. Of the 12 such second year bull market periods since 1950, the S&P 500 has gained an average of 12.6% and was positive every time (

Figure 1).

A gain of this magnitude seems very reasonable at this point, if not conservative, given the potential for support from the Fed as inflation falls. And the S&P 500 is up over 8% since the bull market turned one on October 12, 2023, leaving the index just 4% or so away from that historical average.

Also, consider year one of this bull brought an underwhelming 21.6% gain in the S&P 500 compared to the more than 40% historical average for a first-year bull, leaving some additional upside even after a more than 20% advance in 2023.

The technical backdrop for U.S. equity markets continues to improve. The S&P 500 has staged an impressive comeback after briefly entering a correction period this fall. Broad-based buying pressure outside of just the mega-cap space likely has underpinned the recovery. The cyclical or offensive tilt in market leadership and building momentum in this rally provide additional technical evidence for a sustainable bull market in 2024 characterized by broader participation.

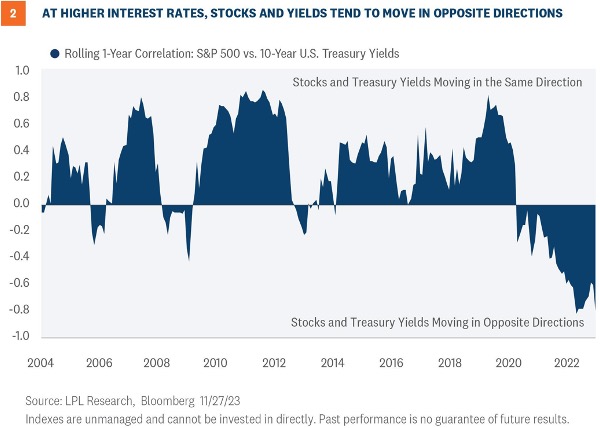

STOCK-BOND CORRELATION MAY BECOME OUR FRIEND

With inflation still somewhat elevated, we cannot completely discount the possibility of renewed upward pressure on interest rates. However, if inflation moves down near the Fed’s target over the course of 2024 as we expect, stocks should benefit.

Stocks and bond yields became increasingly negatively correlated (moving in opposite directions) in 2023 (

Figure 2), which could present an opportunity for stocks and bonds in 2024. LPL Research expects the 10-year Treasury yield to end 2024 between 3.75% and 4.25%, with potential downside if the U.S. economy slows more than economists currently anticipate.

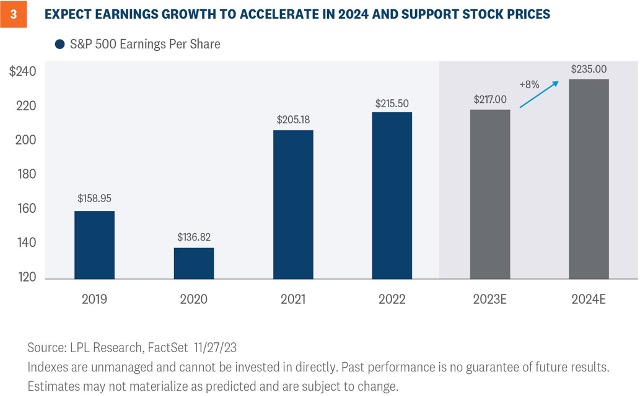

EARNINGS ENTERING A SWEET SPOT

EARNINGS ENTERING A SWEET SPOT

Earnings are exiting a recession and entering a period of growth. But the much better-than- expected bottom-line results from corporate America in 2023 — clearly beneficiaries of the surprisingly resilient U.S. economy — have raised the bar for 2024.

Still, modest economic growth in 2024, in our view, will be sufficient to drive earnings growth in 2024, even if the economy contracts at some point during the year and as long as inflation continues to fall. Our 2024 S&P 500 earnings per share (EPS) forecast is $235 per share, about 7% above the current 2023 consensus S&P 500 EPS estimate of $219 and 8% above LPL Research’s $217 forecast (the long-term historical average earnings growth rate is about 8%,

Figure 3).

How companies manage waning pricing power as inflation falls is key to the earnings outlook. Investors have reason to believe companies will manage this transition well based on what corporate America delivered last quarter. Easy comparisons for healthcare and natural resources and powerful fundamental tailwinds for the technology sector in artificial intelligence and the cloud will help drive a pickup in earnings overall.

UPSIDE POTENTIAL VERSUS DOWNSIDE RISK

Our just-released year-end 2024 fair value target range for the S&P 500 is 4,850–4,950. That range is based on: 1) a next 12 months price-to-earnings ratio (P/E) of 19.5, in line with the five- year average and current levels using the FactSet-tracked consensus earnings estimate; and 2) our projected 2025 S&P 500 EPS of $250, just 6% above our 2024 earnings estimate.

The strong rally since our

Outlook 2024 was published leaves only about 5% upside for the S&P 500 next year (excluding dividends). These returns are not particularly compelling compared to potential returns from fixed income, which carries less risk. However, we do see potential upside above 5,000 if lower interest rates support higher valuations and the U.S. economy avoids recession in 2024, which could enable double-digit earnings growth, as currently reflected in consensus estimates.

What may hold the stock market back? Primarily valuations. The good news is that stocks can potentially move higher in the coming year on earnings gains, without much help from valuations. But sustaining a valuation multiple of over 20 may require our inflation and interest rate forecasts to be too high.

Higher valuations from here would likely also require geopolitical risks not to escalate, so we must continue to watch the Middle East, Russia, and China closely. We don’t expect inflation to reaccelerate or rates to rise, but those risks cannot be completely discounted.

Finally, some volatility during the months leading up to the presidential election next November due to the policy uncertainty would be completely normal.

For more on LPL Research’s 2024 outlook for the economy and markets, please see our just- released

Outlook 2024: A Turning Point.

INVESTMENT CONCLUSION

LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) recommends a neutral tactical allocation to equities, with a modest overweight to fixed income funded from cash. The risk-reward trade-off between stocks and bonds still looks relatively balanced to us even after the strong seven-week rally, with core bonds providing a yield advantage over cash. Favorable seasonality may carry this momentum into January, but we would look for market volatility to pick up a bit at some point during the first quarter as an economic slowdown comes into view and the bond rally potentially runs out of gas.

The STAAC recommends large cap growth-style equities over their large cap value counterparts. The STAAC believes that growth-style large-cap equities may benefit from lower inflation and stabilization of interest rates in the intermediate term. Growth stocks may also benefit from superior earnings prospects against a backdrop of a slowing economy.

Within fixed income, the STAAC recommends an up-in-quality approach with benchmark-level interest rate sensitivity. We think core bond sectors (U.S. Treasuries, agency mortgage-backed securities (MBS), and short-to-intermediate maturity investment grade corporates) are currently more attractive than plus sectors (high-yield bonds and non-U.S. sectors) with the exception of preferred securities, which look attractive after having sold off this spring due to stresses in the banking system.

Ocean City Financial Group

Mark R. Reimet CFP®

801 ASBURY AVENUE

SUITE 650

OCEAN CITY, NJ 08226

609-814-1100 Office

[email protected]

OceanCityFinancialGroup.com

Securities and advisory services offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC. LPL Financial and Ocean City Financial Group are separate entities.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability.

Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency

Not Bank/Credit Union Guaranteed

Not Bank/Credit Union Deposits or Obligations

May Lose Value

RES-000347-1123 | For Public Use | Tracking #517663 (Exp. 12/2024)

For a list of descriptions of the indexes referenced in this publication, please visit our website at lplresearch.com/definitions.