Quincy Krosby, Ph.D.,

Chief Global Strategist, LPL Financial

On October 16, China will begin its 20th National Congress of the Chinese Communist Party in Beijing. This plenum is especially significant because it is expected that President Xi Jinping will be granted an unprecedented third term, something that he set in motion in 2018 when term limits were abolished.

BIG TEST FOR PRESIDENT XI

Analysts anticipate President Xi will further consolidate his power base by ensuring that his political loyalists are appointed positions within the Politburo structure. Because the congress convenes every five years, those moving into the higher ranks are among the leadership cohort that will emerge as China’s senior ruling class. Given the country’s weak economy, due in large part to stringent zero-COVID-19 measures that have led to strict and prolonged lockdowns, coupled with a debt-laden property market, authorities in Beijing and throughout the Chinese provinces will need to focus on reviving the country’s economic underpinning. Moreover, the 20th national congress will most likely be assessing, and perhaps even debating, the trajectory of its future as it seeks military dominance in East and Southeast Asia, technological leadership, and an economy that embraces both capitalism and authoritarianism.

THE ECONOMIC GIANT FACES A REAL ESTATE MELTDOWN

Modern China grew at a dizzying pace as it embarked on opening its economy to the West. Market reforms, trade with the West, and allowing foreign investment led to an economic boom that was characterized by the World Bank as “the fastest sustained expansion by a major economy in history.” China’s trade relationship with the United States grew at such a rapid pace that it became the chief manufacturer of most imported goods. At the same time, U.S. financial services companies, automobile manufacturers, and leading national brands worked towards negotiating agreements to partner with Chinese companies.

Similarly, Chinese entities, especially real-estate companies, invested throughout the U.S. and Europe. But much of China’s expansion in real estate domestically and abroad was fueled by enormous debt that ultimately led to bailouts and various forms of receivership by the Chinese government.

The real-estate industry in China is vast and includes intricate partnerships within other industries. According to Moody’s, the entirety of the industry is responsible for over a quarter of China’s nearly $17 trillion economy. Since early 2022, as cracks in the real estate market became more severe, Moody’s downgraded 91 high-yield Chinese property developers.

Evergrande, a major property developer with vast holdings throughout the country, was placed on Moody’s “B3 negative list.” The list underscores the speculative and high-risk environment that hovers over much of the property market. Given its size and complex relationships across industries, Evergrande exemplifies the depth of the heavily indebted real estate industry. In December, Evergrande defaulted on its debt along with other real estate developers, while many others continue to have trouble making interest payments on time. With over $300 billion in debt obligations, Evergrande’s foreign investors hold approximately $20 billion in notes. More worrisome are the billions of dollars in dollar-denominated debt issued by other Chinese developers.

In addition, over the past year and a half, individual investors have refused to pay monthly mortgage fees on condos in unfinished buildings. Property values continue to fall and indicate few signs of abating. To provide a modicum of assistance, policy banks have been lowering five-year mortgage rates, and one-year prime rates are also being eased in an effort to provide relief to builders who cannot secure private financing. The People’s Bank of China (PBOC), China’s central bank, is also trying to help by allowing cities that are most vulnerable to the property crisis to cut mortgage rates for first-time buyers.

Consequently, if the endemic problems of the industry are not resolved, there are fears that China could undergo its own version of the sub-prime mortgage collapse that engulfed markets globally 14 years ago.

THE EFFECTS OF THE ZERO-COVID-19 POLICY ON CHINA’S ECONOMY

At the end of September, the World Bank downgraded its 2022 economic growth projections for China to 2.8% from an earlier forecast of 5%. Global investment banks are also lowering their GDP estimates. For the first time in 30 years, China’s economic growth is lagging the rest of the Asia-Pacific region. World Bank data expects the other 24 countries encompassing the area to grow a cumulative average of 5.3%. China’s stringent measures to control the spread of COVID-19, the “zero-COVID” policy, are being blamed for the marked slowdown of the world’s second largest economy. Business leaders hope that the upcoming plenum will result in a significant easing, if not a full abolishment of the strategy.

Doubts are growing, however, that President Xi is prepared to abandon the policy that includes mass testing, extreme tracking, and isolating areas where there are outbreaks. Shanghai, with a population of 25 million residents, was shut down for two months this past spring. The restrictions stemming from the shutdown exacerbated global supply chain challenges given the region’s economic importance, but also included disturbing reports of citizens worried about food supplies. And throughout China, lockdowns and quarantines have created an environment of uncertainty with regard to business planning, investing, hiring, or borrowing, not to mention anxiety for the general population.

There is mounting concern that President Xi views his zero-COVID-19 policy, and its ability to eradicate the virus, as a key goal for the country and his platform. That it is increasingly perceived that he remains wedded to maintaining the strict measures clearly indicates that it takes precedence over economic considerations.

SEPTEMBER’S ECONOMIC ACTIVITY INDICATES CONTINUED WEAKNESS—AND THE NEED FOR MORE STIMULUS IS APPARENT

China’s continued economic weakness spilled over into the services sector last month, where intensifying problems in the property market and continued lockdowns are slowing activity in the retail, food services, and transportation sectors. The National Bureau of Statistics reported that the sub-index that measures services fell to 48.9 in September from 51.9 in August. Manufacturing, however, improved slightly.

Weakening global demand presents a major headwind for China as an important exporter to the world. In August, the statistics bureau reported a continuing decline in exports, with new export orders weakening in September. Cargo and container activity for export shipments contracted by 15% compared with a year ago. Expectations are that if a global recession does unfold, the economy will contract more dramatically.

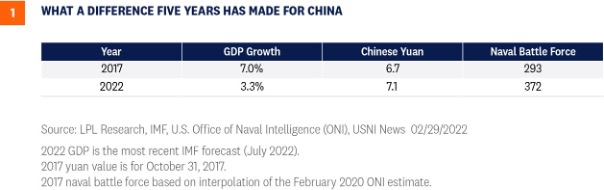

Compared with the previous national congress in 2017, where economic growth stood at 7.0%, the multitude of problems facing party members this year is far greater, while the global backdrop does little to offer help [Figure 1]. Much is expected from this year’s meeting in terms of stimulus, programs for development, and viable solutions to the debt overhang that permeates nearly all sectors of the economy.

CONCLUSION

CONCLUSION

As global central banks struggle to thwart rising inflationary pressures by raising interest rates, the PBOC has lowered rates to help its struggling economy. Expectations for infrastructure projects are most likely to be announced during the congress. Also, with technology expertise within all sub-sectors a top priority, there will probably be comments about how technology is transforming the economy and the country at large.

But economic considerations aside, the continued build-up in the Chinese military highlights that the very top priority for Chinese leadership, where dominance in the region is paramount and military overtures towards Taiwan continue on a daily basis, military spending will not shrink despite the towering problems inherent in the domestic economy. Early in its rapid modern growth period, leaders referred to the country as the Peaceful Giant. Today, under President Xi’s authority, it sounds like an anachronism. In the West, any leader with such a dismal economic record would likely be voted out, and even in many authoritarian regimes, there would likely be popular revolts to topple leaders.

Clearly, the goals in China are starkly different. Keeping the population from uprising has been a fundamental priority since Tiananmen Square. In essence, the contract with the population is that they will be taken care of (the COVID-19 policy is considered to be an integral part of this contract by Xi) in exchange for a compliant population.

To Western observers, it seems incomprehensible that the zero-COVID-19 policies would continue without a leadership change, but the military strength registered under the Xi regime is decidedly more important than the economic weakness wrought by the severe lockdowns.

Over the next five years, China will likely be forced to focus on fixing its domestic problems as it tries to balance its capitalist designs with its inherent authoritarian posture. Although the Peaceful Giant has long ago now left the stage, the world is watching to see what the plans are for the next phase of China’s transformation.

Investors are anxiously awaiting the results of the plenum, as they are every five years. Given the challenging global backdrop accompanied by market volatility, it would be prudent to wait for reports stemming from the meeting to see in which direction China is headed. LPL Research maintains a cautious view of emerging markets equities.

Ocean City Financial Group

Mark R. Reimet CFP®

801 ASBURY AVENUE

SUITE 650

OCEAN CITY, NJ 08226

609-814-1100 Office

[email protected]

OceanCityFinancialGroup.com

Securities and advisory services offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC. LPL Financial and Ocean City Financial Group are separate entities.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency

Not Bank/Credit Union Guaranteed

Not Bank/Credit Union Deposits or Obligations

May Lose Value

RES-1284151-0922 | For Public Use | Tracking # 1-05332879 (Exp. 10/2023)

For a list of descriptions of the indexes and economic terms referenced, please visit our website at

lplresearch.com/definitions.