To Learn More, Be Sure to Visit - oceancityfinancialgroup.com

Quincy Krosby, PhD, Chief Global Strategist Lawrence Gillum, CFA, Chief Fixed Income Strategist Joshua Cline, Associate Analyst As the Federal Reserve (Fed) continues with its Quantitative Tightening (QT) program, questions abound regarding the Treasury Department’s expanding funding needs. The QT program is designed to reduce the Fed’s balance sheet — now $7.7 trillion down from $9 trillion — after Treasury notes (mostly) were bought after economic concerns intensified during the COVID-19-related pandemic. Households and, perhaps surprisingly, foreign investors have been buyers recently, and with the amount of Treasury supply coming to market, both will need to keep buying.

According to recent data from the congressional budget office (CBO), total Treasury debt held by the public is expected to grow to over $46 trillion by 2033. The primary reason for the increase in expected debt issuance is an increase in spending. Per the CBO, the U.S. government is expected to run sizable deficits over the next decade in the tune of 5%–7% of Gross Domestic Product (GDP) each year. So, to fund those deficits, the Treasury Department needs to issue debt. And Treasury plans to issue a lot of debt. And, thus, the Treasury needs buyers.

At this point, the Fed is no longer a buyer of Treasuries. Pension funds, mutual funds, retail portfolios, institutional portfolios, and an assortment of exchange traded funds have been important domestic buyers. Foreign buyers continue to remain active buyers participating in Treasury auctions, but global central banks have not been as active in Treasury auctions as they once were.

With the national debt standing at $34.23 trillion and expected to grow, U.S. Treasury sales are the key to paying the carrying costs. Each auction is heavily monitored by fixed income and equity markets alike to see where the yield settles, as higher yields have a more negative effect on the overall economy.

As the Federal Reserve (Fed) continues with its Quantitative Tightening (QT) program, questions abound regarding the Treasury Department’s expanding funding needs. The QT program is designed to reduce the Fed’s balance sheet — now $7.7 trillion down from $9 trillion — after Treasury notes (mostly) were bought after economic concerns intensified during the COVID-19-related pandemic. Households and, perhaps surprisingly, foreign investors have been buyers recently, and with the amount of Treasury supply coming to market, both will need to keep buying.

According to recent data from the congressional budget office (CBO), total Treasury debt held by the public is expected to grow to over $46 trillion by 2033. The primary reason for the increase in expected debt issuance is an increase in spending. Per the CBO, the U.S. government is expected to run sizable deficits over the next decade in the tune of 5%–7% of Gross Domestic Product (GDP) each year. So, to fund those deficits, the Treasury Department needs to issue debt. And Treasury plans to issue a lot of debt. And, thus, the Treasury needs buyers.

At this point, the Fed is no longer a buyer of Treasuries. Pension funds, mutual funds, retail portfolios, institutional portfolios, and an assortment of exchange traded funds have been important domestic buyers. Foreign buyers continue to remain active buyers participating in Treasury auctions, but global central banks have not been as active in Treasury auctions as they once were.

With the national debt standing at $34.23 trillion and expected to grow, U.S. Treasury sales are the key to paying the carrying costs. Each auction is heavily monitored by fixed income and equity markets alike to see where the yield settles, as higher yields have a more negative effect on the overall economy.

Source: LPL Research, Bloomberg 02/14/24

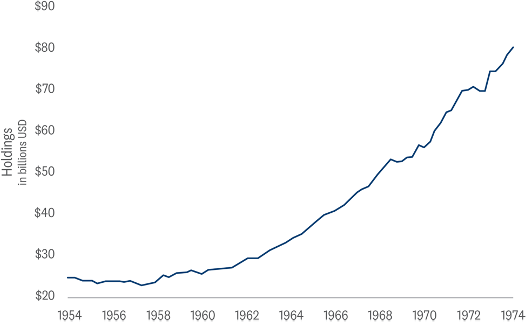

Resorting to an assortment of monetary measures in the Fed’s “toolbox” has been normalized and institutionalized, but a key aspect of these extraordinary purchases is that the Fed will reduce its balance sheet to pre-crisis levels, as it is currently engaged in.

From 1941–1951, the Fed kept rates at low levels to weaken the cost of the debt incurred and subsequently kept the peg in place for six years following the end of World War II. This policy was also implemented during World War I, as well as the war’s aftermath.

Source: LPL Research, Bloomberg 02/14/24

Resorting to an assortment of monetary measures in the Fed’s “toolbox” has been normalized and institutionalized, but a key aspect of these extraordinary purchases is that the Fed will reduce its balance sheet to pre-crisis levels, as it is currently engaged in.

From 1941–1951, the Fed kept rates at low levels to weaken the cost of the debt incurred and subsequently kept the peg in place for six years following the end of World War II. This policy was also implemented during World War I, as well as the war’s aftermath.

Source: LPL Research, St. Louis Federal Reserve 02/14/24

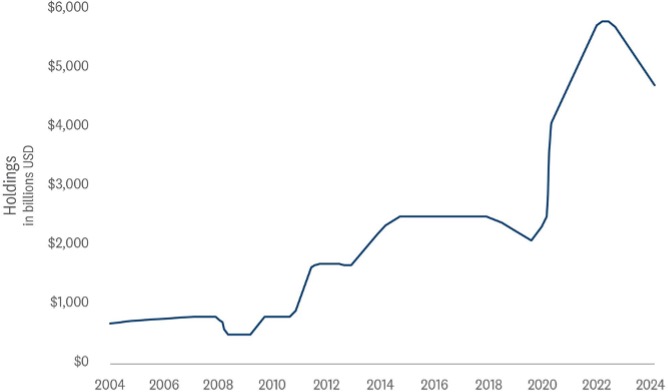

But with the amount of Treasury debt that will likely come to market over the next few years (few decades?), the Treasury department will likely need to find additional demand. The current Treasury buyer base is diverse, with non-domestic buyers and the Fed serving as the largest owners of Treasury securities. However, the largest owner of Treasuries, the Fed, is shrinking its sizable balance sheet and is letting $60 billion of Treasury securities roll off each month (though debt that matures above the $60 billion threshold is currently being reinvested in Treasury securities). Currently, the Fed owns slightly more than $5 trillion in Treasury securities, or roughly 25% of issuance, but is on pace to reduce its exposure by several trillion by the end of 2024. While the Fed will likely not be able to get its balance sheet back to pre-COVID-19 levels, it likely won’t be a large buyer of Treasury securities in the near term either (unless an unforeseen macro event causes the Fed to implement quantitative easing again). So, the biggest buyer of Treasuries is likely on the sidelines for now.

Source: LPL Research, St. Louis Federal Reserve 02/14/24

But with the amount of Treasury debt that will likely come to market over the next few years (few decades?), the Treasury department will likely need to find additional demand. The current Treasury buyer base is diverse, with non-domestic buyers and the Fed serving as the largest owners of Treasury securities. However, the largest owner of Treasuries, the Fed, is shrinking its sizable balance sheet and is letting $60 billion of Treasury securities roll off each month (though debt that matures above the $60 billion threshold is currently being reinvested in Treasury securities). Currently, the Fed owns slightly more than $5 trillion in Treasury securities, or roughly 25% of issuance, but is on pace to reduce its exposure by several trillion by the end of 2024. While the Fed will likely not be able to get its balance sheet back to pre-COVID-19 levels, it likely won’t be a large buyer of Treasury securities in the near term either (unless an unforeseen macro event causes the Fed to implement quantitative easing again). So, the biggest buyer of Treasuries is likely on the sidelines for now.

Source: LPL Research, Bloomberg 02/13/24

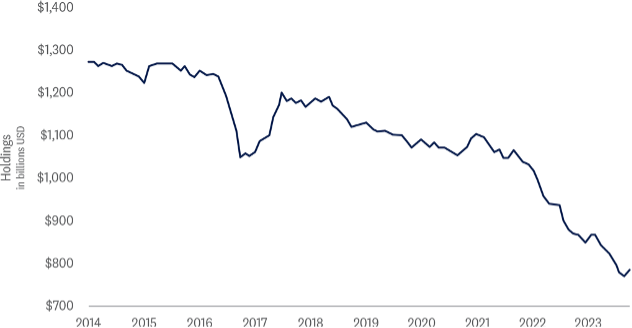

Today, the BOJ is still the largest foreign owner of Treasuries, but they have been less active over the last few years as hedging costs have climbed higher. Moreover, there are concerns that once the BOJ dismantles the Yield Curve Control (YCC) mechanism that keeps their 10-year bond within a band and proceeds with a rate hike as deflation has been defeated, the Japanese could steadily sell their U.S. holdings and repatriate funds back to Japan to take advantage of higher yields.

Source: LPL Research, Bloomberg 02/13/24

Today, the BOJ is still the largest foreign owner of Treasuries, but they have been less active over the last few years as hedging costs have climbed higher. Moreover, there are concerns that once the BOJ dismantles the Yield Curve Control (YCC) mechanism that keeps their 10-year bond within a band and proceeds with a rate hike as deflation has been defeated, the Japanese could steadily sell their U.S. holdings and repatriate funds back to Japan to take advantage of higher yields.

Source: LPL Research, Bloomberg 02/13/24

Many global central banks, including the PBOC, have become active buyers of gold as geopolitical concerns, in concert with an ongoing unwinding of globalization, have deterred buyers from entering recent Treasury auctions.

Source: LPL Research, Bloomberg 02/13/24

Many global central banks, including the PBOC, have become active buyers of gold as geopolitical concerns, in concert with an ongoing unwinding of globalization, have deterred buyers from entering recent Treasury auctions.

Ocean City Financial Group

Mark R. Reimet CFP®

801 ASBURY AVENUE

SUITE 650

OCEAN CITY, NJ 08226

609-814-1100 Office

[email protected]

OceanCityFinancialGroup.com

Securities and advisory services offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC. LPL Financial and Ocean City Financial Group are separate entities.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability.

Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency

Not Bank/Credit Union Guaranteed

Not Bank/Credit Union Deposits or Obligations

May Lose Value

RES-000662-0124 | For Public Use | Tracking #542691 (Exp. 02/2025)

For a list of descriptions of the indexes referenced in this publication, please visit our website at lplresearch.com/definitions.

Ocean City Financial Group

Mark R. Reimet CFP®

801 ASBURY AVENUE

SUITE 650

OCEAN CITY, NJ 08226

609-814-1100 Office

[email protected]

OceanCityFinancialGroup.com

Securities and advisory services offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC. LPL Financial and Ocean City Financial Group are separate entities.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability.

Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency

Not Bank/Credit Union Guaranteed

Not Bank/Credit Union Deposits or Obligations

May Lose Value

RES-000662-0124 | For Public Use | Tracking #542691 (Exp. 02/2025)

For a list of descriptions of the indexes referenced in this publication, please visit our website at lplresearch.com/definitions.