To Learn More, Be Sure to Visit - oceancityfinancialgroup.com

Quincy Krosby, PhD, Global Macro Strategist, LPL Financial Jeffrey Buchbinder, CFA, Chief Equity Strategist, LPL Financial A lot has changed in the past few weeks, both in terms of expectations for interest rates and lost confidence in the health of the banking system as a result of the sharp rise in interest rates that has led to some things “breaking,” as we wrote about here last week. Here we share some thoughts on who’s to blame for the ongoing banking crisis and reiterate how we are telling investors to adjust, or not adjust, their asset allocations in light of ongoing market volatility.

MARKETS ON ALERT

It’s difficult to grasp that just a few weeks ago, the fed funds futures market had priced the terminal rate at nearly 6%. The market’s hawkish outlook was predicated on the Federal Reserve (Fed) raising rates amid a still solid economy underpinned by a tight labor market and consumer spending, but with inflation still above the 2% level that reflects price stability.

Now, with continued pressure on both domestic and global banks, markets are expecting the Fed will be forced to cut rates towards the end of this year as loan growth slows and businesses, particularly small businesses, and consumers find it more difficult to secure loans. As a result, the broader economy is expected to be negatively affected.

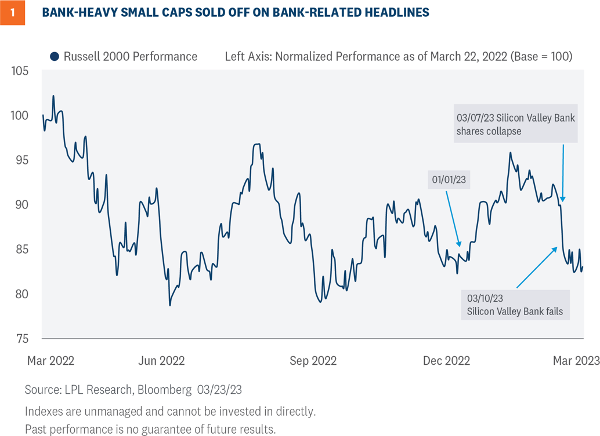

The rapid collapse of Silicon Valley Bank (SVB), followed by continued pressure on regional banks, along with headlines surrounding the struggle to shore up confidence in First Republic Bank (FRC), has the market on alert for other potentially vulnerable banks. The banking stress of the past couple of weeks has put some heavy pressure on the bank-heavy small cap Russell 2000 Index (Figure 1).

A lot has changed in the past few weeks, both in terms of expectations for interest rates and lost confidence in the health of the banking system as a result of the sharp rise in interest rates that has led to some things “breaking,” as we wrote about here last week. Here we share some thoughts on who’s to blame for the ongoing banking crisis and reiterate how we are telling investors to adjust, or not adjust, their asset allocations in light of ongoing market volatility.

MARKETS ON ALERT

It’s difficult to grasp that just a few weeks ago, the fed funds futures market had priced the terminal rate at nearly 6%. The market’s hawkish outlook was predicated on the Federal Reserve (Fed) raising rates amid a still solid economy underpinned by a tight labor market and consumer spending, but with inflation still above the 2% level that reflects price stability.

Now, with continued pressure on both domestic and global banks, markets are expecting the Fed will be forced to cut rates towards the end of this year as loan growth slows and businesses, particularly small businesses, and consumers find it more difficult to secure loans. As a result, the broader economy is expected to be negatively affected.

The rapid collapse of Silicon Valley Bank (SVB), followed by continued pressure on regional banks, along with headlines surrounding the struggle to shore up confidence in First Republic Bank (FRC), has the market on alert for other potentially vulnerable banks. The banking stress of the past couple of weeks has put some heavy pressure on the bank-heavy small cap Russell 2000 Index (Figure 1).

The swift crash of Signature Bank, the third largest bank failure in U.S. history, following the demise of SVB, which held $160 billion in deposits, along with Silvergate Bank, has investors and depositors questioning if the banking system is as “sound and resilient with strong capital and liquidity” as suggested recently by both Fed Chair Jerome Powell and Secretary of the Treasury Janet Yellen.

To be sure, the Fed’s emergency bank lending facility, the Bank Term Funding Program, which was quickly put in place to help strengthen the banks, also served to restore confidence as banks grapple with depositors who are seeking higher rates elsewhere, and who are also increasingly concerned about the viability of the banks themselves.

The swift crash of Signature Bank, the third largest bank failure in U.S. history, following the demise of SVB, which held $160 billion in deposits, along with Silvergate Bank, has investors and depositors questioning if the banking system is as “sound and resilient with strong capital and liquidity” as suggested recently by both Fed Chair Jerome Powell and Secretary of the Treasury Janet Yellen.

To be sure, the Fed’s emergency bank lending facility, the Bank Term Funding Program, which was quickly put in place to help strengthen the banks, also served to restore confidence as banks grapple with depositors who are seeking higher rates elsewhere, and who are also increasingly concerned about the viability of the banks themselves.

Ocean City Financial Group

Mark R. Reimet CFP®

801 ASBURY AVENUE

SUITE 650

OCEAN CITY, NJ 08226

609-814-1100 Office

[email protected]

OceanCityFinancialGroup.com

Securities and advisory services offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC. LPL Financial and Ocean City Financial Group are separate entities.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability.

Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency

Not Bank/Credit Union Guaranteed

Not Bank/Credit Union Deposits or Obligations

May Lose Value

RES-1471350-0323 | For Public Use | Tracking # 1-05365330 (Exp. 3/2024)

For a list of descriptions of the indexes referenced in this publication, please visit our website at lplresearch.com/definitions.

Ocean City Financial Group

Mark R. Reimet CFP®

801 ASBURY AVENUE

SUITE 650

OCEAN CITY, NJ 08226

609-814-1100 Office

[email protected]

OceanCityFinancialGroup.com

Securities and advisory services offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC. LPL Financial and Ocean City Financial Group are separate entities.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability.

Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency

Not Bank/Credit Union Guaranteed

Not Bank/Credit Union Deposits or Obligations

May Lose Value

RES-1471350-0323 | For Public Use | Tracking # 1-05365330 (Exp. 3/2024)

For a list of descriptions of the indexes referenced in this publication, please visit our website at lplresearch.com/definitions.