Winning a large customer order is often a defining moment for a startup. It validates product-market fit and signals real demand. Yet for many early-stage companies, that same order exposes a critical problem: fulfilling it requires capital the business does not yet have.

Inventory, manufacturing, raw materials, logistics, or supplier deposits must often be paid upfront, while customer payments may arrive weeks or months later. For startups without deep cash reserves or access to bank credit, this gap can stall growth at the moment it should accelerate.

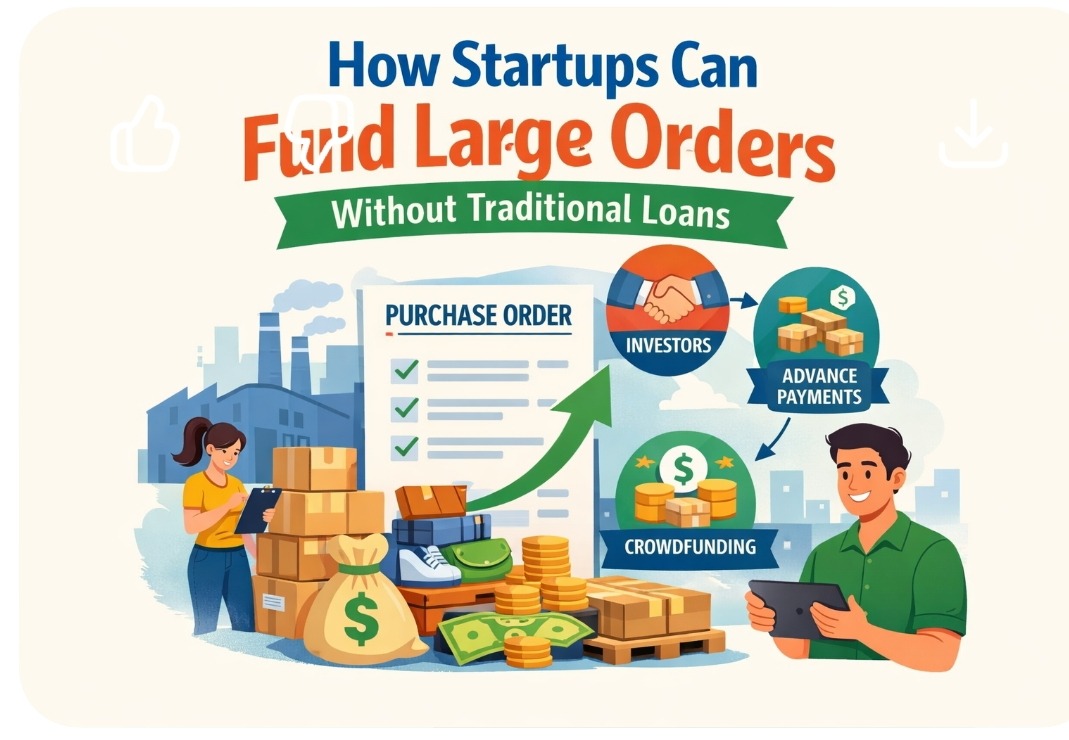

Fortunately, funding large orders does not always require traditional loans.

Conventional bank financing is designed around historical performance, collateral, and creditworthiness. Startups frequently fall short on all three.

Banks typically require:

Even when a startup qualifies, approval timelines are slow, and loan structures add long-term debt, often an unattractive tradeoff for a short-term fulfillment need.

Most startups that struggle with large orders do not lack customers. They lack timing alignment between expenses and payments.

Suppliers and manufacturers expect payment before or during production. Customers, especially enterprise buyers, operate on net-30, net-60, or longer payment terms. The startup is forced to finance the gap.

This mismatch is structural, not operational, and it requires financing solutions built around transactions rather than credit history.

Purchase order (PO) financing is designed to solve one of the most common growth constraints startups face: the inability to fund production or supplier costs after winning a large order but before receiving customer payment. Unlike traditional loans, PO financing is tied to a specific transaction rather than the company’s balance sheet.

Once a startup receives a confirmed purchase order from a customer, a PO financing provider advances funds directly to the supplier to cover manufacturing, inventory, or fulfillment costs. This allows the startup to move forward with the order without exhausting cash reserves or seeking long-term debt.

PO financing focuses on the strength of the transaction rather than the startup’s operating history. Approval is typically based on three core factors:

After the goods are produced and delivered, the startup issues an invoice to the customer. At that point, the transaction is settled either through direct customer payment or through invoice factoring, which accelerates cash collection.

Purchase order financing is not a universal solution, but it is highly effective under the right conditions. It works best for startups that:

PO financing is widespread in manufacturing, wholesale distribution, import/export, consumer goods, and industrial supply chains, industries where upfront costs are significant and payment cycles are extended.

For startups that have already delivered goods or services, invoice factoring addresses the next phase of the cash flow cycle. Instead of waiting 30, 60, or 90 days for customer payment, the startup sells its invoice to a factoring company and receives most of the invoice value upfront.

The factoring company then collects payment directly from the customer and releases the remaining balance to the startup, minus agreed-upon fees. This structure allows startups to convert receivables into working capital without taking on traditional debt.

Many startups use PO financing and invoice factoring together as part of a continuous cash flow strategy rather than isolated tools.

By combining the two, startups can fund large orders end-to-end, from supplier payment to customer collection, without waiting through extended payment cycles. This approach allows founders to accept larger contracts, fulfill them confidently, and reinvest cash into operations and growth.

Order-based financing is transaction-specific. Funding is tied to individual purchase orders or invoices rather than adding long-term liabilities to the balance sheet.

Approval is driven by customer strength and deal structure, making these solutions accessible to startups without extensive operating history or strong personal credit.

Unlike equity financing, order-based financing does not require founders to give up ownership or control.

As order volume increases, available funding grows in line with revenue, creating a flexible financing model that adapts to business growth.

Order-based financing is powerful, but it is not suitable for every business model. It generally does not work well for:

PO financing and factoring also require coordination with suppliers and customers, which may feel unfamiliar to early-stage founders. Understanding these constraints is essential when evaluating fit.

Funding large orders without traditional loans is possible, but it requires aligning financing with how the business actually operates. Startups built around purchase orders and invoices can often access capital by leveraging customer demand rather than relying on credit history.

The key insight is that growth financing does not always mean borrowing. For the right startup, order-based financing can turn opportunity into execution, without adding long-term debt or sacrificing equity.